Beranda

/ Insurance Expense Credit Or Debit / Debit note vs credit note in insurance explained ... - A debit is an accounting transaction that increases either an asset account like cash or an expense account like utility expense.

Insurance Expense Credit Or Debit / Debit note vs credit note in insurance explained ... - A debit is an accounting transaction that increases either an asset account like cash or an expense account like utility expense.

Insurance Gas/Electricity Loans Mortgage Attorney Lawyer Donate Conference Call Degree Credit Treatment Software Classes Recovery Trading Rehab Hosting Transfer Cord Blood Claim compensation mesothelioma mesothelioma attorney Houston car accident lawyer moreno valley can you sue a doctor for wrong diagnosis doctorate in security top online doctoral programs in business educational leadership doctoral programs online car accident doctor atlanta car accident doctor atlanta accident attorney rancho Cucamonga truck accident attorney san Antonio ONLINE BUSINESS DEGREE PROGRAMS ACCREDITED online accredited psychology degree masters degree in human resources online public administration masters degree online bitcoin merchant account bitcoin merchant services compare car insurance auto insurance troy mi seo explanation digital marketing degree floridaseo company fitness showrooms stamfordct how to work more efficiently seowordpress tips meaning of seo what is an seo what does an seo do what seo stands for best seotips google seo advice seo steps, The secure cloud-based platform for smart service delivery. Safelink is used by legal, professional and financial services to protect sensitive information, accelerate business processes and increase productivity. Use Safelink to collaborate securely with clients, colleagues and external parties. Safelink has a menu of workspace types with advanced features for dispute resolution, running deals and customised client portal creation. All data is encrypted (at rest and in transit and you retain your own encryption keys. Our titan security framework ensures your data is secure and you even have the option to choose your own data location from Channel Islands, London (UK), Dublin (EU), Australia.

Insurance Expense Credit Or Debit / Debit note vs credit note in insurance explained ... - A debit is an accounting transaction that increases either an asset account like cash or an expense account like utility expense.. Unexpired insurance premiums are reported as prepaid insurance (an asset account). When the asset is eventually consumed, it is charged to expense.if consumed over multiple periods, there may be a series of corresponding charges to expense. Accrued means owed or owing. accrued expenses is a liability account.it means expenses that are owing or payable. An insurance expense occurs after a small business signs up with an insurance provider to receive protection cover. Money taken from your account to cover expenses.

A prepaid expense is an expenditure paid for in one accounting period, but for which the underlying asset will not be consumed until a future period. After making the entry, the balance of the unused service supplies is now at $600 ($1,500 debit and $900 credit). In each business transaction we record, the total dollar amount of debits must equal the total dollar amount of credits. From the table above it can be seen that assets, expenses, and dividends normally have a debit balance, whereas liabilities, capital, and revenue normally have a credit balance. Expense $150 of the insurance with a debit.

Analyzing revenue, expense, and withdrawal transactions ... from i.ytimg.com When reviewing your insurance policy whether it's for your home, auto or business, it's important to understand the factors that can add or subtract to the premium. Expense $150 of the insurance with a debit. So before answering, let's make sure we really understand what accrued expenses are. Accrued expenses are similar to accounts payable. In general, only debits are entered in expense types of accounts. Money coming into your account. The initial journal entry for a prepaid expense does not affect a company's financial statements. Insurance expense is part of operating expenses in the income statement.

Now, moving onto the question put up by you expense is a debit or a credit? applying the above mentioned modern rule of accounting i believe the answer to your question is that it's a debit.

If the retailer has incurred some insurance expense but has not yet paid the premiums, the retailer should debit insurance expense and credit insurance premiums payable. Insurance expense is part of operating expenses in the income statement. When the asset is charged to expense, the journal entry is to debit the insurance expense account and credit the prepaid insurance account. From the table above it can be seen that assets, expenses, and dividends normally have a debit balance, whereas liabilities, capital, and revenue normally have a credit balance. So before answering, let's make sure we really understand what accrued expenses are. By identifying the type of account (asset, liability etc.) and establishing which side of the accounting equation it is on (left or right), it is possible to determine. Debits and credits total debits must always equal total credits accounting books: Money coming into your account. Expense types of accounts are the easiest to understand with bookkeeping. When reviewing your insurance policy whether it's for your home, auto or business, it's important to understand the factors that can add or subtract to the premium. After making the entry, the balance of the unused service supplies is now at $600 ($1,500 debit and $900 credit). Accounts general journal general ledger (t account) chart of accounts. Accrued expenses are similar to accounts payable.

Insurance expense journal entry at the end of each month, the company usually make the adjusting entry for insurance expense to recognize the cost of that has expired during the period. Accrued means owed or owing. accrued expenses is a liability account.it means expenses that are owing or payable. The initial journal entry for a prepaid expense does not affect a company's financial statements. In general, only debits are entered in expense types of accounts. A $135 debit to prepaid insurance.

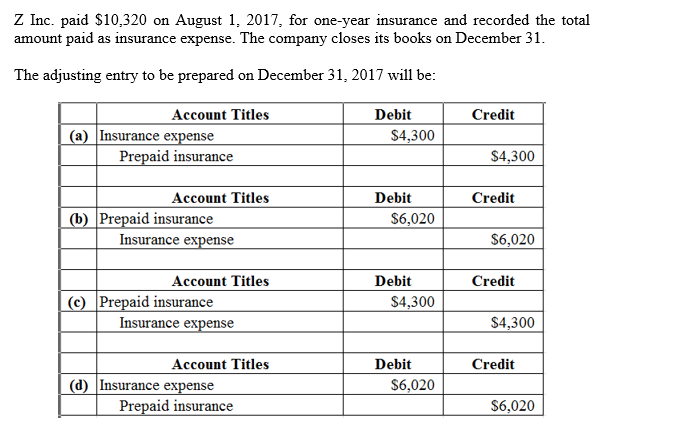

Answered: Z Inc. paid $10,320 amount paid August… | bartleby from prod-qna-question-images.s3.amazonaws.com Now, we've achieved our goal. The debits and credits mentioned in the question above are a bit confusing. Thus, the amount charged to expense in an accounting period is only the amount of the prepaid insurance asset ratably assigned to that period. Likewise, the company can make insurance expense journal entry by debiting insurance expense account and crediting prepaid insurance account. Expense types of accounts are the easiest to understand with bookkeeping. I) rent expense, with a balance of $19,000 was omitted from the trial balance. Now, moving onto the question put up by you expense is a debit or a credit? applying the above mentioned modern rule of accounting i believe the answer to your question is that it's a debit. Insurance agreements last for a certain period of time.

If, for example, you have a debit of $1,000 from the purchase of a new computer, you would then create an equal credit for the asset of the computer.

Likewise, the company can make insurance expense journal entry by debiting insurance expense account and crediting prepaid insurance account. A debit is an accounting transaction that increases either an asset account like cash or an expense account like utility expense. Companies may incur expenses through cash or credit purchases. Accounts general journal general ledger (t account) chart of accounts. For example, refer to the first example of prepaid rent. I) rent expense, with a balance of $19,000 was omitted from the trial balance. Accrued means owed or owing. accrued expenses is a liability account.it means expenses that are owing or payable. Assets = liabilities + equity the accounting equation must always be in balance and the rules of debit and credit enforce this balance. After making the entry, the balance of the unused service supplies is now at $600 ($1,500 debit and $900 credit). The insurance provider charges an annual fee, called a premium, which will cover the business for 12 months. Repeat steps 1 through 4 for the other. Money taken from your account to cover expenses. On the other hand, the insurance expense account will have a debit balance of $50 reflecting the expired portion of the insurance policy during january.

There are now a few final expense companies have finally caught on and accept the direct express cards as a valid form of payment which also happen to be some of the best final expense. In general, only debits are entered in expense types of accounts. A debit is an accounting transaction that increases either an asset account like cash or an expense account like utility expense. Almost all health insurance companies accept credit and debit cards as acceptable payment, but only a limited number companies will take them for life insurance. Accrued expenses are similar to accounts payable.

How to debit and credit prepaid insurance and the ... from lh3.googleusercontent.com A $135 debit to prepaid insurance. Insurance agreements last for a certain period of time. So before answering, let's make sure we really understand what accrued expenses are. Expired insurance premiums are reported as insurance expense. Accrued expenses are not expenses. When reviewing your insurance policy whether it's for your home, auto or business, it's important to understand the factors that can add or subtract to the premium. After all debits and credits are posted to the general ledger, the prepaid insurance account will have a debit balance of $550 reflecting the cost of insurance policy that has not expired. Before delving into the debits and credits for expense accounts, there is some accounting terminology to understand.

Repeat steps 1 through 4 for the other.

From the table above it can be seen that assets, expenses, and dividends normally have a debit balance, whereas liabilities, capital, and revenue normally have a credit balance. Expense accounts rarely have credit entries posted to them. The amount paid to acquire a specific coverage is known as premium. Now, moving onto the question put up by you expense is a debit or a credit? applying the above mentioned modern rule of accounting i believe the answer to your question is that it's a debit. To record insurance expense, a bookkeeper debits the insurance expense account and credits the insurance payable account. Only the expired portion of the premium should be presented as insurance expense. If, for example, you have a debit of $1,000 from the purchase of a new computer, you would then create an equal credit for the asset of the computer. For example, refer to the first example of prepaid rent. When reviewing your insurance policy whether it's for your home, auto or business, it's important to understand the factors that can add or subtract to the premium. Thus, the amount charged to expense in an accounting period is only the amount of the prepaid insurance asset ratably assigned to that period. Combine your answer from step 2 and step 3 to find whether you debit or credit the account you identified in step 1. After all debits and credits are posted to the general ledger, the prepaid insurance account will have a debit balance of $550 reflecting the cost of insurance policy that has not expired. One of the factors is the use of your financial credit or credit score to rate your insurance risk.